From the cost of medication to education to everyday expenses, the Biden administration has passed several laws and implemented many federal rules taking on giant corporations, but big businesses are fighting tooth and nail to protect their profits.

Since taking office in 2021, the Biden administration has passed a series of laws and issued several regulations in an effort to crack down on corporate exploitation of workers and consumers, put more money back into families’ pockets, and level the playing field for working- and middle-class Americans.

But, as with anything having to do with money, big businesses and corporations are resisting efforts to reign in their power, filing a series of lawsuits intended to stop or reverse some of these new laws and regulations.

Let’s break them all down.

- Medicare Drug Price Negotiations

- Noncompete Clauses

- Overtime Pay

- Medical Billing on Credit Reports

- Credit Card Late Fees

- Overdraft Fees

- Other Surprise and Scam Fees

Medicare Drug Price Negotiations

President Biden’s Inflation Reduction Act authorized Medicare to negotiate prices for expensive drugs with pharmaceutical companies for the first time, lowering costs for seniors. The law will also penalize drug companies for price increases that exceed the rate of general inflation.

The first negotiations, which are currently underway, will include the blood thinners Eliquis and Xarelto, as well as the diabetes drugs Jardiance, Januvia, and Farxiga, and Novo Nordisk’s suite of insulins, which go by the names Fiasp and NovoLog.

The negotiated prices will go into effect in 2026 and save up to nine million seniors money on prescription drugs, according to the White House.

Another 15 drugs will be selected for negotiation and see their prices decrease in 2027, with 15 more following in 2028, and 20 more in 2029 and each year afterwards.

These new price negotiations aim “to basically make drugs more affordable while also still allowing for profits to be made,” Gretchen Jacobson, who researches Medicare issues at the Commonwealth Fund, said in August.

The Congressional Budget Office reports that the new Medicare negotiation provision will save taxpayers $160 billion by reducing how much Medicare pays for drugs through negotiation and inflation rebates.

This isn’t stopping pharmaceutical giants from mounting a vigorous legal battle against the negotiation provision, however.

In a series of lawsuits, companies like Merck have blasted the initiative, calling it unconstitutional and defending their high prices. They claim that the regulation could undermine future cures. Lawyers for Bristol Myers Squibb, Janssen, Novartis, and Novo Nordisk also offered several objections to the negotiations earlier this year, saying that they constitute “the illegal taking of their drugs.” Other companies have claimed even signing a contract would be unconstitutional, because it would force them to admit publicly that a lower price is a fairer price.

The Medicare drug price negotiation program survived its first court challenge by a drugmaker in March, after a federal judge ruled against AstraZeneca in a lawsuit the company filed challenging the program.

Other legal proceedings remain ongoing.

Noncompete Clauses

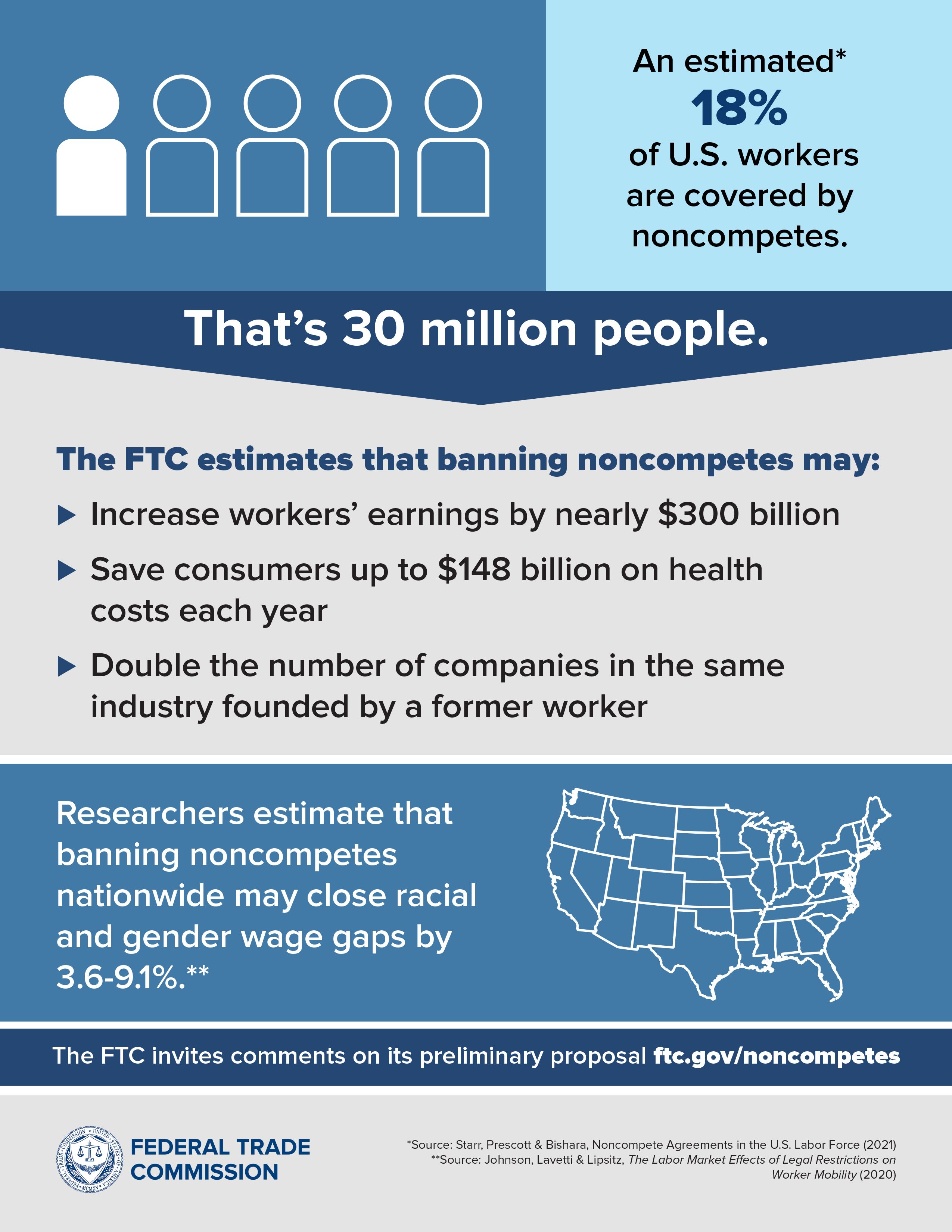

In April, the Federal Trade Commission (FTC) voted to ban noncompete agreements—clauses that employers often force their workers to sign which effectively bar them from starting their own business or finding a new job in the same field within a certain area or timeframe after leaving their current job.

An estimated 30 million American workers are currently affected by noncompete clauses—roughly 18% of the US workforce. These clauses have been shown to lower workers’ pay and restrict their opportunity and mobility.

The final rule bans new noncompete agreements for the vast majority of American workers and requires employers to let current and past employees know they won’t enforce them going forward. Companies will now also be required to throw out existing noncompete agreements for most of their employees.

The FTC argues the rule will boost workers’ economic freedom and estimates that the rule will boost workers’ wages by up to $488 billion over the next decade, with earnings for the average American worker increasing by an additional $524 per year under the new rule.

The new rule is scheduled to go into effect 120 days after it’s published in the Federal Register. The future of the rule is uncertain, however, as pro-business groups have already begun taking legal action to prevent its implementation.

The US Chamber of Commerce and the Business Roundtable filed a lawsuit against the agency in federal court in the Eastern District of Texas in April. Chamber President and CEO Suzanne Clark called the FTC vote “a blatant power grab that will undermine American businesses’ ability to remain competitive.”

Another lawsuit was filed in federal court in the Northern District of Texas by business tax services firm Ryan, a company owned by a Republican mega donor and tax adviser to former president Donald Trump.

Overtime Pay

In April, the Biden administration announced a new rule to expand overtime pay for around four million lower-paid salaried employees nationwide. The regulation will increase salary thresholds required to make workers exempt from overtime pay laws.

In other words, salaried employees who work more than 40 hours per week and make under a certain amount annually—at a higher threshold than before—will be required to receive overtime pay from their employers. The new rule does not change standards for hourly employees, who are already protected by overtime regulations.

The present annual threshold for salaried employees’ overtime pay is around $35,500, set by the Trump administration in 2019. Beginning on July 1, 2024, that cutoff will increase to $43,888. It will further increase to $58,656 on Jan. 1, 2025.

The Labor Department estimates that this new rule will ensure that nearly 30% of full-time salaried workers in the United States are eligible for overtime pay, as opposed to the existing standards put in place by former President Donald Trump, under which only 15% of these workers are eligible.

The proposal would have the greatest impact on workers in the retail, food, hospitality, and manufacturing industries.

In another major change, the proposed rule would use wage data to implement automatic updates to the salary level for overtime eligibility every three years. The rule would also help ensure that more low-paid salary workers and workers in US territories receive overtime protections.

These changes will take effect on July 1.

Although labor advocates have praised the rule, business groups have claimed that the policy change will “unreasonably drive up payroll costs” and some have warned that they plan to challenge the rule legally.

In May, a coalition of business groups including the National Federation of Independent Business, the International Franchise Association, and the National Retail Federation filed a lawsuit seeking to block the rule. These groups state that the rule “will force many smaller employers and non-profits operating on fixed budgets to cut critical programming, staffing, and services to the public.”

Medical Billing on Credit Reports

The Biden administration announced last year that it would develop federal rules that would bar unpaid medical bills from affecting patients’ credit scores.

Barring medical bills from appearing on credit reports would help tens of millions of Americans who have medical debt by eliminating information that can depress their scores, and therefore make it more difficult for them to get a job, rent an apartment, or secure a car loan, for example.

Hospital leaders and representatives of the debt collection industry oppose the rule, however, and claim it may have unintended consequences, such as more hospitals and physicians possibly having to require upfront payment before delivering care. These groups have also warned that looser credit requirements could also make it easier for consumers to get loans they may never pay back.

Previously, following pressure from the federal government, the three major credit rating agencies, Equifax, Experian, and TransUnion, also began removing small, unpaid medical bills and debts that were less than a year old from consumer credit reports. This has led to a significant drop in total medical debt nationwide, according to an analysis from the nonprofit Urban Institute.

As of August 2023, 5% of American adults with a credit report had a medical debt on their report, down from almost 14% from two years prior. The analysis also found that Americans with medical debt on their credit report saw their VantageScore—a credit score jointly developed by the three major credit bureaus to predict how likely you are to repay borrowed money— improve from an average of 585 to 615, which moved many of these consumers out of a subprime category. Subprime borrowers usually have higher interest rates on loans and credit cards, if they’re able to borrow money at all.

In total, about 27 million Americans experienced a significant improvement in their score, Urban Institute researchers estimated.

Despite the wide-ranging benefits of efforts to tackle medical debt, a California dermatologist sued the three major credit rating agencies last year, claiming that if medical debts don’t appear on credit reports, patients will have less of an incentive to pay their bills, which could potentially cost physicians billions of dollars. That case is still pending in federal court.

Credit Card Late Fees

In March, the Biden administration announced a federal rule that would cap most credit card late fees at $8.

The rule would apply to “large” credit card issuers – those that have more than one million open accounts, such as American Express, Discover, and Capital One. According to the Consumer Financial Protection Bureau (CFPB), these large issuers represent more than 95% of the total outstanding credit card debt in the United States.

The rule also aims to close a loophole that has allowed credit card companies to “exploit” certain borrowers by allowing them to raise fees on those who made late payments, the CFPB says.

The CFPB estimates that the final regulation would save American families more than $10 billion a year by cutting fees from an average of $32. The agency also estimated that the over 45 million Americans who are charged late fees on credit cards each year would save an average of $220 annually.

Shortly after the Biden administration’s announcement of the rule in March, however, the American Bankers Association (ABA) and the US Chamber of Commerce filed a legal challenge.

The rule was set to go into effect in mid-May, but a Trump-appointed federal judge in Texas blocked the rule, granting an injunction sought by the banking industry and other business interests to freeze the restrictions while the legal challenges play out.

The Biden administration expressed disappointment with the decision, saying that the Texas court sided with “Republicans, big banks, and special interests.”

Legal analysts have said that the fight isn’t over, however, and that the case could reach the US Supreme Court.

Overdraft Fees

Earlier this year, the CFPB also proposed a rule that would curb excessive overdraft fees charged to American consumers of large banks and credit unions, which could potentially save consumers as much as $3.5 billion a year.

Overdraft fees are charged when a deposit account holder’s transaction is covered by their bank or credit union because there isn’t enough money in that person’s account.

The CFPB has found that customers “are typically charged $35 for an overdraft loan, even though the majority of consumers’ debit card overdrafts are for less than $26, and are repaid within three days.” The agency also estimates that roughly 23 million households a year pay overdraft fees and that the proposed rule could save each household $150 a year.

The rule would also require lenders to be more forthcoming about the terms of extending an overdraft loan.

This rule would only apply to banks and credit unions with at least $10 billion in assets, which account for the largest share of deposit account customers in the country.

Financial institutions immediately pushed back against the CFPB’s announcement, and have been fighting back with a “multimillion-dollar marketing and lobbying campaign,” according to the Associated Press.

“The proposal would make it significantly harder for banks to offer overdraft protection to customers, including those who have few, if any, other means to access needed liquidity. The CFPB is effectively proposing to take away overdraft protection from consumers who want and need it,” American Bankers Association President and CEO Rob Nichols said in a statement to CNN.

Other Surprise and Scam Fees

More broadly, the Biden administration has taken a number of actions aimed at ending corporate price-gouging and junk fees—those pesky, extra charges that companies tack onto purchases at checkout, which are usually significantly higher than the initially advertised price.

In October, the Biden administration proposed a new rule that would prohibit companies across the private sector from hiding additional fees from consumers.

The proposed FTC rule would require all industries under its jurisdiction to show the full price of an item being purchased to the consumer “up-front,” meaning before they get to checkout. The rule would apply to concert and sports tickets, apartment and car rentals, hotel rooms, and more.

Companies that violate the proposed rule would be subject to financial penalties and be required to compensate consumers.

Several US airlines, including American, Delta, and United, are suing to block this rule, as they claim it would “confuse consumers by giving them too much information during the ticket-buying process,” according to the Associated Press. As a result of the legal action, the rule has yet to be implemented.

The Biden administration proposed a new regulation last summer that would require cable companies and satellite providers to show the full price of their services “upfront”—meaning hidden fees would no longer be snuck in at checkout. This rule went into effect in March.

Ticketmaster, SeatGeek, and other major ticketing companies have also agreed to institute “all-in” pricing under pressure from the Biden administration, which would also mean that consumers will no longer be surprised by additional fees at checkout.

Since then, the Biden administration has filed a lawsuit against Live Nation, the parent company of Ticketmaster, alleging that the company violated antitrust laws in order to create a monopoly over the live events industry in the United States.

The FTC also announced that it was suing Amazon last year, alleging that the company tricked millions of people into signing up for Prime service through “deceptive user interface designs.” The complaint also alleges that Amazon tried to keep users subscribed—even when they wanted to cancel their memberships—by making it exceedingly difficult to unsubscribe. That trial is set for Oct. 2026.

{kind=link}